"IULs Are Risky.” Myth… or Convenient Misinformation?

- Heritage

- Mar 3

- 1 min read

You’ve probably heard it before.

“Too complicated.”

“Too market-dependent.”

“Too good to be true.”

But let’s slow down and separate noise from facts.

Here’s What People Think Is Risky

Most assume that because an Indexed Universal Life (IUL) references a market index, your money is directly invested in the stock market.

That’s not how it works.

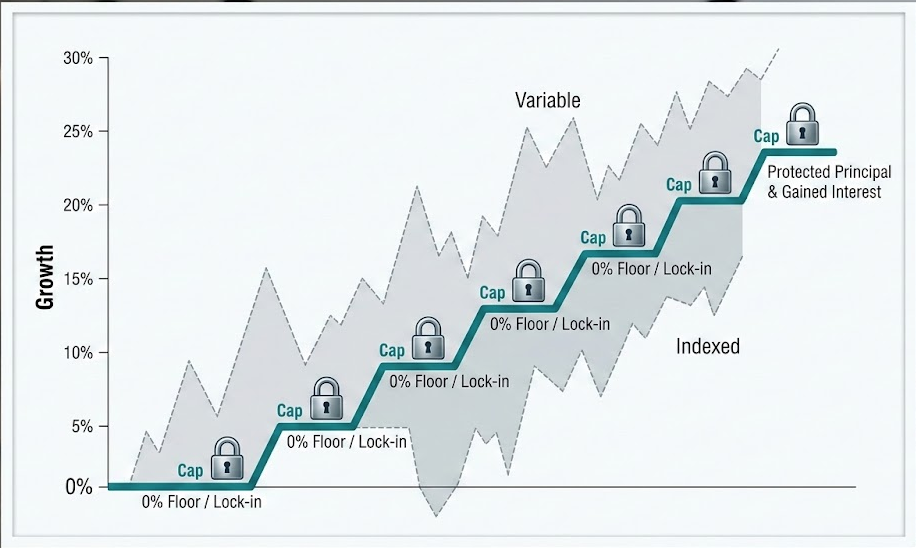

IULs are designed with downside protection. In most structures:

When the index goes up, you participate up to a cap.

When the index goes down, you’re typically protected by a floor (often 0 percent).

So the real question isn’t “Is it risky?”

But do you understand how it’s structured?

Let's dive into some more.

Where the Real Risk Actually Is

The “risk” isn’t usually the market.

The risk is:

Poor design.

Overfunding or underfunding.

High internal costs not explained properly.

Working with someone who doesn’t structure it strategically.

An IUL isn’t magic. It’s a financial tool.

And like any tool, in the wrong hands it can be inefficient. In the right structure, it can become:

A tax-advantaged accumulation strategy

A legacy tool

A supplemental retirement income vehicle

A liquidity strategy for business owners

The Bigger Question

What’s riskier?

A properly structured IUL with a floor and defined parameters…

Or relying entirely on volatile market exposure without protection?

Or worse — not having a strategy at all?

If you’ve heard IULs are “risky,”you deserve to see the math; not just the opinion.

Because when you understand how the staircase actually works, fear turns into clarity.

Let’s have the real conversation.

Comments